Budgets are tough. Tough to follow and tough to create. Just when you think you have your budget under control, an unexpected expense throws it off balance. Experience a few surprises within a month, and it can be easy to throw your hands up in frustration and go rogue on the budget.

But the good news—budgets can be as flexible or as detailed as you want them to be. While some find a strict budget helpful (think zero-based budgets), others are okay with a looser approach.

How detailed should your budget be? Let’s take a look at what goes into a detailed budget and see if it works for you.

What is a detailed budget?

Detailed budgets spell out specific categories, such as groceries, gas, and electricity, and allocate a fixed amount to each one. At the very extreme, they give every dollar a name and purpose, preventing you from spending outside the rigid limits you create.

How can you create a detailed budget?

Some budgeters get very detailed with their budgets, breaking categories (say, groceries) into uber-specific subcategories (meat, vegetables, dairy). Others simply list broadly their expenses and allocate a dollar amount based on previous spending. But, in essence, most detailed budgets separate expenses into three big categories: fixed, variable, and irregular expenses.

1. Fixed expenses

A fixed expense is a recurring cost that doesn’t change from month to month. Consider these the anchors of your budget: you know how much you’ll spend on these expenses, which makes calculating them fairly easy. Fixed expenses you’ll find in a detailed budget include:

- Mortgage payments or rent

- Insurance premiums (car, home, renters, life, health)

- Debt payments

- Internet, cable, and monthly subscriptions

- Daycare or school tuition

- Savings goal

Notice we included a savings goal as a fixed expense. While, yes, you could save a different amount each month, you’ll hit financial goals faster if you treat savings as a fixed expense.

2. Variable expenses

As you can guess, variable expenses are those costs that change from month to month. Variable expenses are the bread and butter of a detailed budget: since you have some control over how much you spend in this area, a detailed budget can keep you from overspending. Common variable expenses include:

- Food (groceries, restaurants, take-out, school lunches, snacks)

- Transportation/gas

- Utilities (gas, electricity, water)

- Entertainment (movies, hobbies, concerts)

- Clothing

- Personal health (haircare, medical, therapy, beauty products)

Sometimes, budgeters will break variable expenses into “essential” and “discretionary” spending. In this way, essentials represent your needs (groceries, for instance) and discretionary expenses represent your wants (movies). This could help you prioritize your spending, especially if you’re saving for something big.

3. Irregular expenses

Finally, no detailed budget is complete without the ever-elusive irregular expenses. Unlike fixed and variable expenses, irregulars aren’t recurring, which makes them easy to forget (hence why some call them “pop-up” costs). Irregular expenses in a detailed budget can include:

- Holiday and birthday gifts

- Car maintenance and repairs

- Home maintenance (pest services, lawn care)

- Taxes

- Vehicle registration

The most detailed budgets will break irregulars into two subcategories, predictable and unexpected. Predictable expenses—such as vehicle registration and taxes—should have a place in your budget, preferably in the month they occur. It’s the unpredictables (surprise car repairs or medical bills) that can make things tricky.

One solution is to set aside a small amount each month for those expenses you can’t predict. If you don’t use the money, you can put it in a separate emergency fund, which becomes the ultimate safety net for big emergencies.

Do you need a detailed budget?

For some budgeters, a detailed budget is exactly what they need to stay on track. With a detailed budget, you know where your money is going, helping you hit tough financial goals, pay debt faster, and prevent you from living a consumption-driven lifestyle.

But they’re not for everyone. For those whose income is variable—small business owners or contractors, for instance—keeping a detailed budget is like shooting a moving target. Just when you think you got it, it shifts.

At the end of the day, the best budget for you is one that actually works. If giving every dollar a name and purpose ends up being a complete waste of time, then a detailed budget may not be the best approach.

What are some alternatives to a detailed budget?

If you find detailed budgets impractical and downright frustrating, don’t worry—you have other options. Here are just three alternatives to a detailed budget.

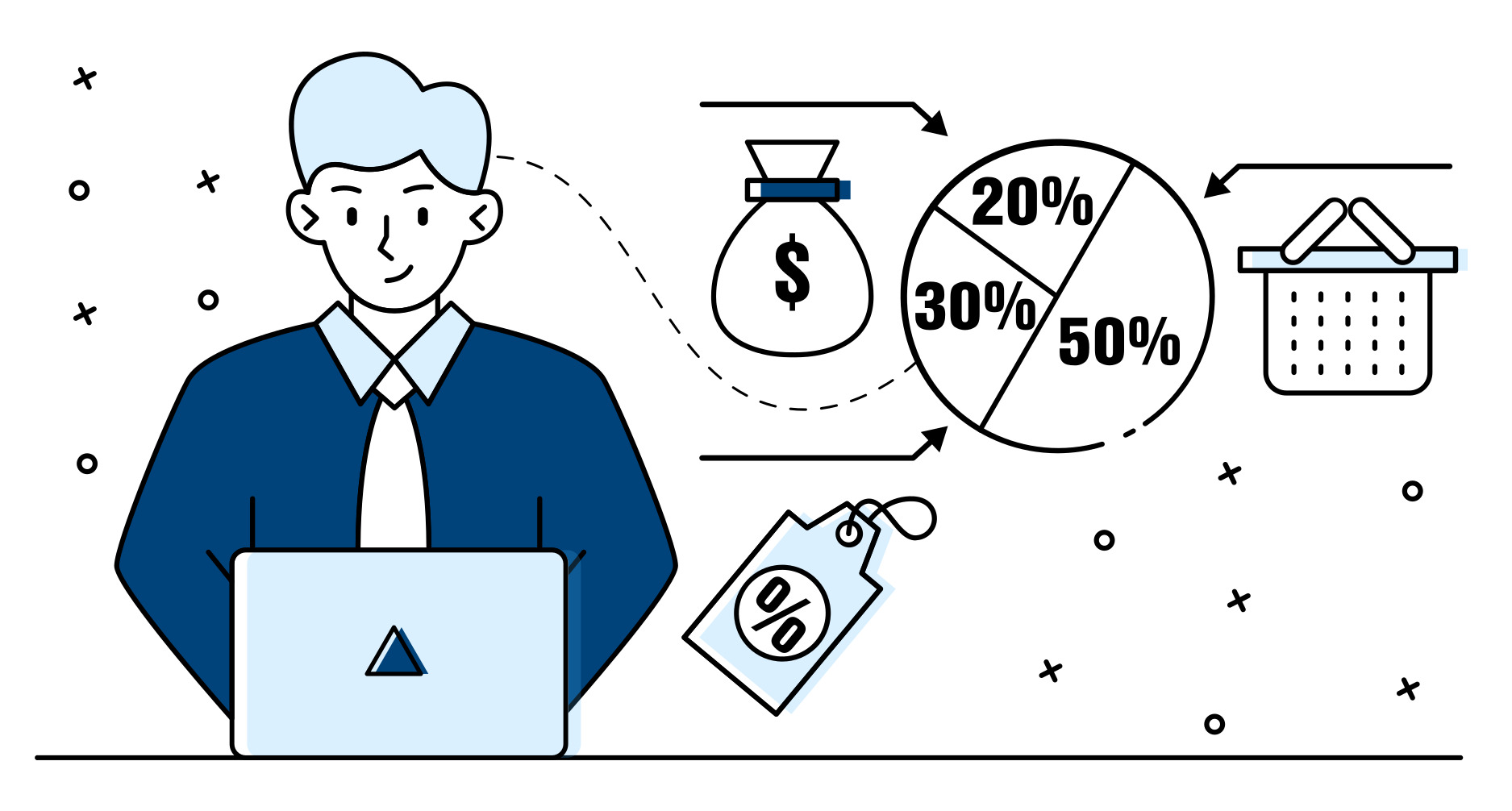

1. The 50/30/20 budget

A 50/30/20 budget is a great alternative if you want some structure, but you want some wiggle-room, too.

It works like this. Every month, you allocate 50% of your take-home pay to essential spending (rent, utilities, groceries, insurance, clothing), 30% to discretionaries (eating out, entertainment), and 20% to savings or debt repayments.

For instance, if you bring home $5,000 per month, a 50/30/20 budget would allocate $2,500 to needs, $1,500 to wants, and $1,000 to savings and debt.

It’s a loose budget. But, if that’s what you’re looking for, a 50/30/20 budget can help you from overspending on one area, as well as ensure you’re always putting money aside for savings.

You can change the ratios, too. Instead of saving only 20%, you could save 35%, turning your budget into a 50/15/35. As long as you have enough to cover your needs, you can adjust the budget to fit your financial goals.

2. The “pay-yourself-first” approach

If a 50/30/20 is too much budgeting, you could try the “pay-yourself-first” approach. Also known as “reverse budgeting” a pay-yourself-first budget starts with a savings goal, then builds a spending plan around it.

Proponents of this approach often automate their savings and essential spending, allowing banks or financial institutions to take out a portion of their paycheck the moment it hits their account. In this way, whatever is left over is money you can spend.

3. The “no” budget

The “no” budget is perhaps the simplest budget you can have. But it can also be the hardest to follow, especially if you have a tendency to overspend. As its name suggests, a “no” budget consists entirely in saying no to purchases you can’t afford.

Here’s how it works. You calculate how much you must spend every month (think mortgage, bills, groceries). You subtract this by what you earn, and what’s left over is money you can use for discretionary expenses, savings, and debt repayment.

In this way, you prioritize essentials before any other expense. And, when your money runs out, you simply say “no” to purchases you can’t afford. If you have the discipline to say no, a “no” budget might be right for you.

For expenses you can’t budget, Stately can help

A detailed budget can help you plan for expected expenses. But not even the most detailed budgeters can predict when an unexpected expense, such as a medical emergency or major home repair, will land on their path.

If you have an emergency fund, you might be able to cover these expenses. But what happens when the emergency is bigger than your emergency fund? Should you take out a credit card, personal loan, or HELOC?

Not so fast. For emergencies you can’t cover, Stately can help.

We offer affordable, low-interest loans with no hidden fees that you pay back through payroll. It’s a super safe way to borrow money, way safer than high-interest loans and credit cards, and because it’s attached to your payroll, you won’t have to worry about missing a payment and damaging your credit.

For small emergencies, use our payroll advance, which gives you money you’ve already earned ahead of payday. Aside from a small origination fee, you’ll pay nothing to get a Stately salary advance. If the emergency is big, our employee loans will give you a low-cost and affordable way to secure the funds you need.

Don’t let an unexpected expense drag you or your budget down. Contact us when emergencies strike, and we’ll be there to help you get through it!